Note: This post is also available in audio format on the Abraham’s Wallet podcast (on iTunes, Google and Spotify).

Let’s take a minute to listen in on an ACTUAL conversation (this is a lie) that was recorded (on, uh… reel to reel papyrus?) between Abraham and his employee Eliphaz (not his real name; his real name was Stan):

A: You wanted to see me Eliphaz? How’s the herd doing this month?

E: Well I’m glad you asked Abraham, that’s actually what I wanted to talk about. I was hoping to be put in charge of a few more sheep. Whaddaya think?

A: I’m open to it; sounds reasonable. How’s the herd doing?

E: Great. The sheep are just fine. And I really feel like I’ve been living “my best life” out there lately. You know, exactly in the right place here and now. Thriving, I guess I’d say!

A: Uh, ok. But I meant, how many healthy, new sheep has your herd produced this month? And… shearing season is upon us; how many pounds of wool do we have so far?

E: Right. Not sure. My focus THIS month has been more about self-care and trying to get a vision for where I’m going with my life. And I’ll tell you, it’s more than a little exciting.

A: …

E: And part of my journey, of course, is working for you, and that’s been the case my entire life, and that’s great. I’m really feeling like I understand your heart for what we’re trying to accomplish here Abraham, and I could not be more excited about taking on more responsibility. Let’s do this.

A: Let me be sure I’m grasping this. I gave you a herd of sheep – I think it was about 200. You don’t know how many of my sheep you’ve got today? And you’re asking for a bigger herd?

E: Okay, pretty much accurate, but I’d include…! …that I’ve been on sheep duty for almost a year now and, though I remain glad for the work and the food and the housing and community and the access to the worship tent and the defense against marauders that your family provides me, frankly… it’s starting to… bother me… that I’ve yet to be entrusted with more sheep. [Pauses, bites lip.] Most of your sheep crew seems to be managing pretty solid herds from what I gather. Shmuel told me he was about to get a herd of Cattle. That kind of hurt, seeing as he’s only been with us since July…

A: Shmuel’s herd increased by 35% in the last 3 months.

E: I hear you Abraham, but I don’t feel like you’re hearing me

A:….. [narrows eyes, wonders if there’s an opening on the Dung Removal patrol]

– – – – – – – – – – – – – – – – – – – – – –

The explicit goal of this website is to equip YOU to be capable and confident of stewarding more (more children, more disciples, more money, etc.). As illustrated in our fabulous, touching, soon-to-be-award-winning Abrahamic drama above, he who cannot give an account of how he has managed what he has should NOT be entrusted with more. (Big definition coming up, get ready…) A BUDGET is a tool for planning and monitoring the financial assets and income streams with which we have been entrusted.

Luke 14:28

Which of you, intending to build a tower, does not sit down first and count the cost, whether he has enough to finish it?

Step One, Pick a tool and confront reality

The first step in creating a budget is knowing your current situation – how much are you spending per month? In order to do this the right way, you’ll need a tool. Glancing over your credit card statements and swagging at your expenditures is not a substitute for precise tracking of every penny that you spend. Pick a tool that will allow you to be very precise with the tracking of your expenses. You will need to track what you actually spend for at least a month. (There are many “outlier” months; several would be better. You’ll travel more in the summer; you’ll spend more on gifts in December, etc.)

Reality is important to this exercise. This is not what you would like to spend – don’t even think about anything other than accurate tracking for the next four+ weeks!

Since most of us are spending as much as possible passively (via automatic payments for mortgage/rent, student loan, credit card, etc.), a tool like Mint makes much more sense than lower-tech tracking methodologies. If that’s not you, feel free to record all of your income and expenses in a spreadsheet or even a notebook, but go that direction with caution. For the rest of us, which tool should you use?

Because of their total dominance in the space, Mint is always my first thought here. I am a loyal Mint user and have spoken with many folks who didn’t like it because they tried it years ago but have returned to find many of their gripes resolved in later versions of the app. I also like Mint due to their longevity. I used to recommend an app called LevelMoney, and they recently shuttered the service after being acquired by Capital One. Getting your budgeting tool to really work perfectly for you does take effort, so I prefer to pick on that I trust will still exist in two or three years.

If you feel like trying out another player, You Need a Budget (YNAB) is a great app that does many things better than Mint. Their biggest advantage is that they FORCE you to account for every dollar in your budget, including savings. They also include a bunch of tools that are better than Mint’s for goal tracking, debt pay down, etc. And their support is far superior to Mint’s. How can they do all of this? Because they charge you $7 per month. I like the app but just don’t see $84 of additional value over Mint, so I’m staying put.

Although I’ve found the benefits of Mint to outweigh the risks, I would be remiss if I didn’t warn you that anytime you hand over logins to your financial accounts to a third party, you’re exposed to some level of risk. Please do your due diligence and decide for yourself if you feel comfortable with services that aggregate your financial data. At some point in the future we’ll do a round up of all of the financial tools and apps that I find helpful or terrible, but for now I’d just pick one that allows you to track every penny you spend for at least 4 weeks. Go do that and return to this post once you’re done. Bye. (If you get bored and just HAVE to scratch that Abraham’s Wallet itch in the meantime, feel free to re-read the hilarious skit above.)

– – – – – – – – – – – – – – –

Step Two, Know where you are

Oh hi again. That last month… what a crazy ride amiright? So you’ve returned with your month of data in hand and you are either feeling like a champ or you’re horrified at the open drain that apparently exists in your financial bathtub. No problem.

Take your data and place it into reasonable big buckets, like housing, groceries, entertainment, etc. If you used an online tool, this might be already done for you. Now consider what isn’t showing up in that budget that you actually do need to be setting aside money towards. For example, you might only pay your car insurance bill every six months, but you didn’t pay it in the past four weeks so we’ll miss a pretty big expense if we don’t account for it. You can also normalize categories where there was a large expense that is infrequent (your fridge broke and you had to replace it, so just estimate what that big bucket of home expenses might be over 12 months with the understanding that a few of these things are bound to happen every year). It’s a bit of work but it’s really worth it. Don’t give up, amigos. Take the time and get it done.

Now step back and look at those big buckets – do they correspond well to your goals and values or would your budget say that the highest good in your life is the mocha chip frappuccino? Matthew 6:21 says “For where your treasure is, there your heart will be also”. Looking at your spending over a month can be a fantastic mirror gazing opportunity for understanding our own hearts. If you need to do business with God and change your heart and ways, you can click HERE for our handy dandy guide for repenting. (No I’m not kidding. Walking through financial issues will inevitably lead you into some good old repentance.)

Step Three, Build a budget

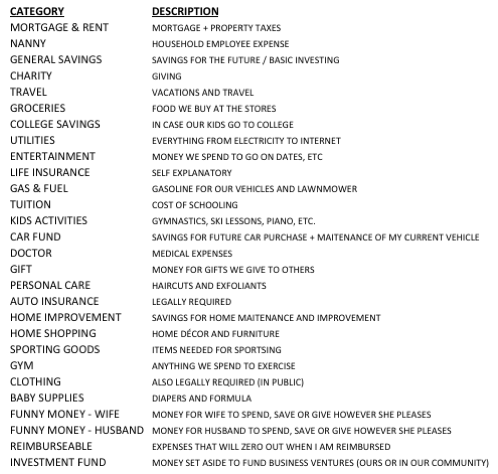

Now we get to the vision part. Figure out which categories work for you. Here’s a snapshot of mine:

There are a few critical checks once you’ve taken your income and slotted it into all of these buckets.

First, budget to zero. You must not create a budget that results in a deficit! I like to go a step further and create a budget that only relies upon the bare minimum that I expect to earn over a time period. Bonuses, tax refunds, etc. are all used as I see fit, if they happen, but we won’t be counting on uncertain cash flows. And as you consider how much to put in each bucket, pay them in order of priority. We’ll cover the prioritization topic in-depth in a later post.

Second, I highly suggest creating rolling buckets in your budget. This allows you to budget for those less frequent expenses easily. I know that I need about $800 ever year to cover my car insurance, so my budget shows $67 monthly for car insurance. At some points in the year that bucket will be very red, and at other times it will be very green, depending on when the expense occurred, but over 12 months I will have budgeted and spent $800.

Third, capture everything. I know many folks who budget only for “the big stuff”. Particularly for high income people, this can be very tempting, but I recommend against it. Part of learning stewardship is getting past the idea of “well now I have plenty so I don’t need to worry about the small stuff”. While it may be wisdom to, for example, trade money for time as your earning potential or assets increase, that does not mean that your dollars got less valuable because you now have more of them. This one is a big fallacy I see amongst even the most devoted Jesus-loving stewards of money. As your assets and income increase, these unaccounted for dollars can start to make up a huge amount of money left unmonitored.

We should all be asking the LORD, “Father, how many of these dollars that you’ve put into my care would you like me to use to treat myself with?”. In my experience, the answer is usually, “some of them”. God has never given me the impression that, due to my increase in wealth, it’s high time to upgrade my perfectly adequate vehicle. I leave you to the counsel of your community and the Holy Spirit to draw lines in this regard, but there it is.

Step Four, Obey thy budget

This step is the hardest, of course. For many people, there will need to be a period of low-tech budget adherence enforcement via legal, paper tender. Dollar bills ya’ll. If you put as many of them in an envelope as you have budgeted for Groceries for a given month, and then write “GROCERIES” on that envelope, you will have created a handy self-enforcing budget device. This works marvelously. As a 20-year-old who had received a cost of living grant to spend the summer studying immigration policy in Texas, I promptly blew most of the grant on a new road bike and learned through necessity that with the help of the local discount grocery, a man can live on $50 per month in groceries. Same idea with the paper envelopes minus the folly of multi-thousand dollar bicycle purchases.

Once you’re comfortable adhering to a budget, you can move beyond the envelope stage and your budgeting tool will become the ‘envelope’. My wife and I take a peek at Mint before every trip to the grocery store (yes, every one. You can call us nerdy but don’t call us cheap. We spend generously and with delight… but we waste none of it, or at least aspire to). That app has become our paper envelope, and when it says we’re tapped for the month, we resort to raiding the pantry. This takes discipline, but we have found no better way to keep our spending in line with our larger values and goals.

To wrap up, you must become proficient at the creation, maintenance and adherence to a budget if you hope to effectively manage and grow money. For most of us, due to finite income, budgeting is also a critical skill necessary for growing a family. Approaching this task as the servant who is eager to show themselves a capable and trustworthy steward is not just mental gymnastics to get you to do your chores – it’s a repositioning of yourself before the Giver Of All Good Things. It’s also a fantastic spot to start a journey towards multigenerational stewardship.

May you become a budgeting maven and wow your friends with your precise acumen around them dollars. This is a foundational skill!

EDIT: Now that we’ve been at this for a while, we’ve got more good stuff for you when it comes to budgeting. Check out our series on how to budget slush here!

BONUS! You Need a Budget founder Jesse Mecham has written a book that echoes exactly what this post says in much greater detail. If you want to go deeper on budgeting, pick up You Need a Budget (the book).

My buddy Dave just came into my office today saying that this article totally framed up where he is right now and he felt convicted before he ever finished the drama at the beginning! How’s that for effective?? Nice one!